In early June, as magnesium prices continued to climb to a high level, buyers gradually returned to rationality. Coupled with the fact that small magnesium plants were selling at low prices, the center of magnesium prices gradually moved downward. Additionally, news of magnesium plant resumptions gradually spread, and the increased supply of magnesium ingots was likely to further increase inventory pressure on magnesium smelters, reopening the downward channel for magnesium prices, which fell back to 15,950 yuan/mt. In mid-to-late June, downstream traders entered the market in concentrated numbers to purchase, providing demand support. Magnesium prices rebounded several times, but due to factors such as lower order prices received earlier, magnesium prices fluctuated rangebound in mid-to-late June.

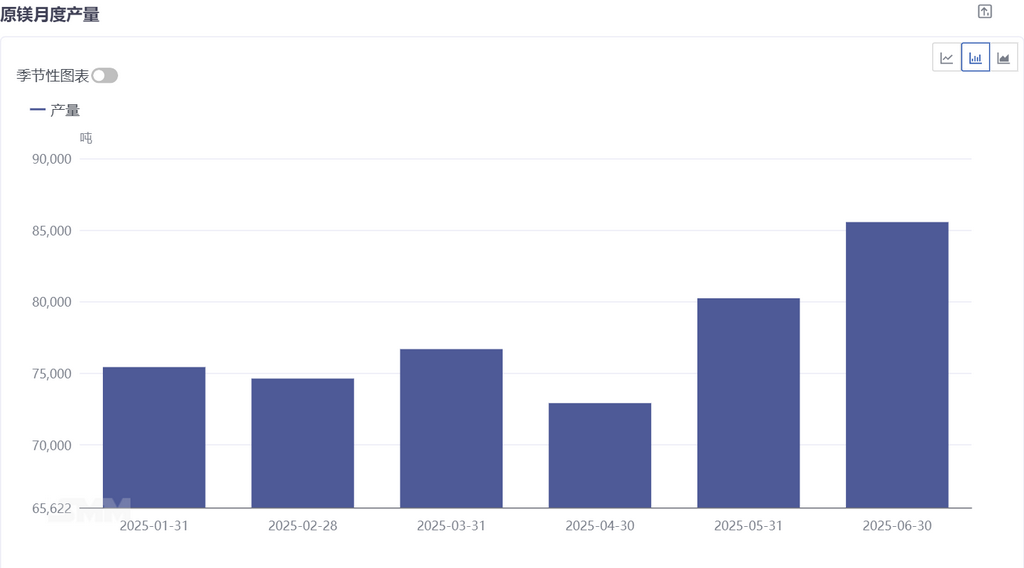

China's primary magnesium production in June 2025 increased by 6.63% MoM. Domestic primary magnesium producers' production volumes varied in June, with an overall increase in nationwide magnesium ingot production MoM. The increase in this month's production was mainly due to the following two reasons: Firstly, due to the decline in raw material prices, the profit margins of primary magnesium smelters effectively improved. Magnesium ingot smelters that had previously halted production due to cost losses gradually resumed primary magnesium production in early June, leading to an increase in primary magnesium production in June. Secondly, two primary magnesium smelters in Xinjiang that had previously undergone maintenance gradually resumed production, which significantly boosted primary magnesium production. The decrease in this month's primary magnesium production was mainly due to the following reason: Two primary magnesium smelters in Shaanxi Province underwent maintenance or production cuts, resulting in a decrease in primary magnesium production of approximately 1,500 mt in June due to these factors. Overall, the increase in nationwide primary magnesium production was greater than the decrease, with an overall 6.63% MoM increase in primary magnesium production in June.

According to the SMM survey, currently, four primary magnesium smelters in the main production areas have reported production resumption plans for July, and one has recently started production. The specific resumption times for other primary magnesium smelters are undetermined, and SMM will continue to monitor. Overall, domestic magnesium ingot smelters' production volumes are likely to increase in July, with an expected slight MoM increase in domestic primary magnesium production in July.

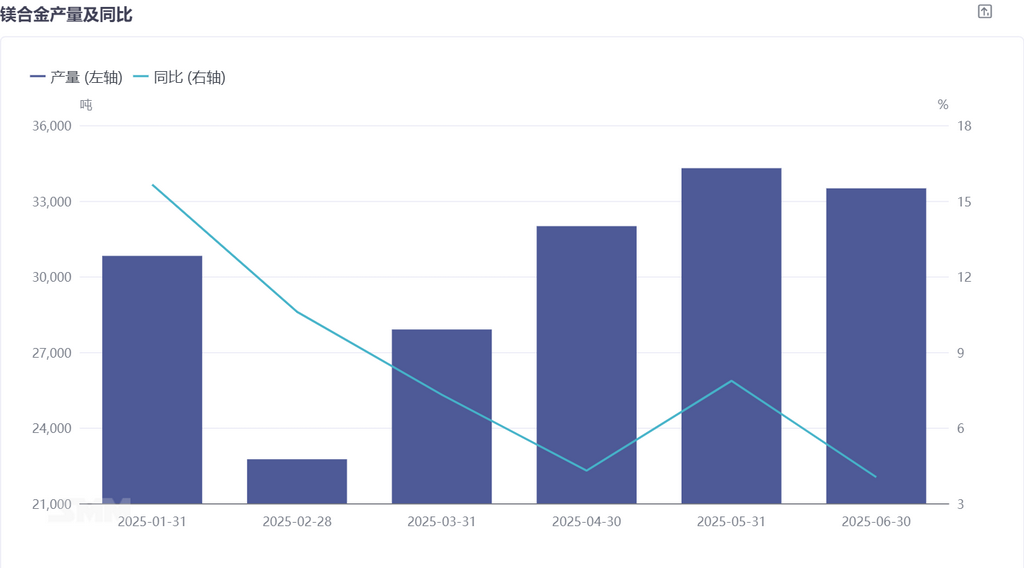

China's magnesium alloy production in June 2025 decreased MoM. Domestic magnesium alloy producers' production volumes continued to increase in June, with the magnesium alloy market showing a fluctuating development trend in recent times. As major producers increased their market promotion efforts, the cost-performance advantage of magnesium alloy materials gradually gained industry recognition, prompting some die-casting enterprises to begin adjusting their production processes and gradually replacing aluminum alloys with magnesium alloys. Although this material substitution trend has not yet resulted in large-scale orders, it has driven a mild increase in overall demand. It is worth noting that June, as a traditional peak production season for the die-casting industry, directly boosted short-term demand for magnesium alloys. However, as seasonal factors shifted, the market began to exhibit off-season characteristics, with procurement volumes pulling back recently. Based on current market supply and demand changes, the industry generally expects magnesium alloy production to moderately decrease in July.

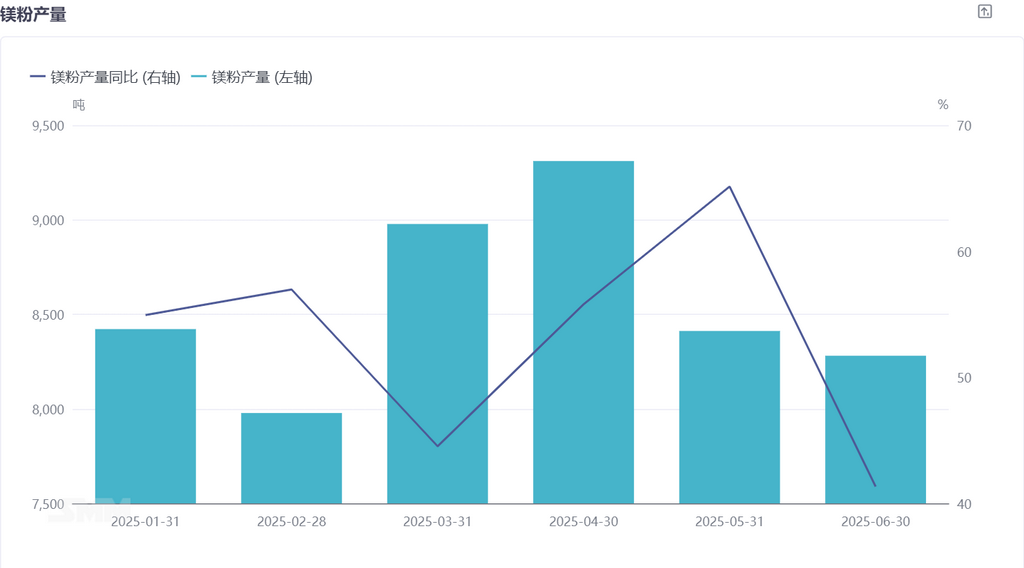

According to data from SMM, China's magnesium powder production in June 2025 decreased by 1.65% MoM. The domestic magnesium powder market in June exhibited characteristics of structural adjustment. Despite facing dual pressures from both domestic and external demand—with the domestic consumer market remaining sluggish and export orders declining for several consecutive months due to shrinking procurement demand from international steel enterprises—the market showed significant differentiation. Some small and medium-sized producers have voluntarily reduced their capacity utilization rates, while leading producers, leveraging their concentrated order advantages, have instead increased their operating levels. This dynamic of one declining while the other rises has narrowed the overall production decline compared to expectations. With the end of the traditional peak season, the market generally expects demand to weaken further, and the industry is likely to face even greater production cut pressures in July.